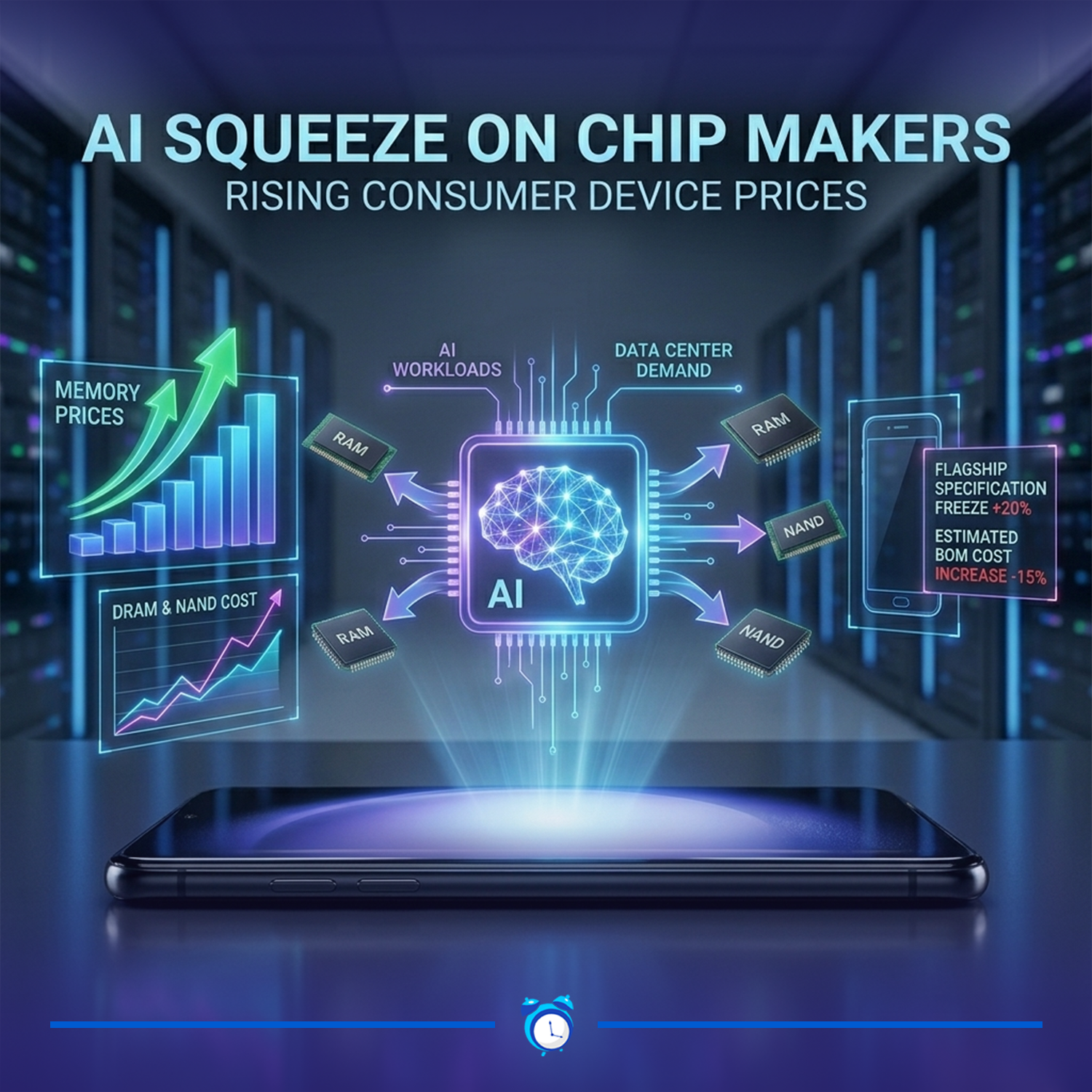

AI exerts pressure on chip makers driving up prices of global electronic devices

The accelerating adoption of artificial intelligence (AI) is causing a transformational shift in every industry and consumer space, changing the way we work, learn, and share ideas. We are witnessing a seamless integration of concepts that were once confined to science fiction into our everyday reality. Numerous enterprises report that their data potentials cannot keep up with their business demands.

However, the rapid expansion of AI infrastructure and workloads is exerting significant pressure on the memory ecosystem. These AI workloads require large amounts of memory, and the shortage, in part, is driven by a reallocation of manufacturing capacity away from consumer electronics toward high-margin memory solutions to support AI.

Instead of expanding conventional DRAM and NAND used in smartphones, PCs, and other consumer electronics, major memory makers have shifted production toward memory used in AI data centers, such as high-bandwidth (HBM) and high-capacity DDR5. This has restricted the supply of general-purpose memory modules and driven up prices across the board.

“We fully agree that prudential standards should remain proportionate to the evolving risk profile of rural banks as they transition toward more technology-enabled operations,” the RBAP said.

“However, we hold strong reservations against the manner in which the digitalization of rural banks is proposed to be carried out,” it added.

Among the concerns raised by RBAP is the BSP’s proposal to classify full digital onboarding capability as an indicator of operational complexity, which could trigger higher prudential requirements. The association said the approach might be too broad and should instead consider whether such capability materially changes a bank’s risk profile.

RBAP also questioned the proposed 30-percent threshold on customer accounts located outside a rural bank’s physical areas of operation. It said the rule may be difficult to implement and could create unintended consequences. The association noted uncertainties over how “physical areas of operations” would be defined, warning that strict geographic limitations could reduce access to formal financial services, especially in border areas or regions with mobile populations.

The Bangko Sentral ng Pilipinas, the nation’s central bank, regulates all banks in the country. Philippine banks are classified as universal, commercial, thrift, rural, cooperative, and Islamic banks. Universal banks offer a wide range of services, including investment, commercial and development banking, mutual funds, and housing loans.

Commercial banks—privately owned institutions—are the largest financial group and most popular among customers for their extensive service offerings. Expanded financial inclusion measures have improved Filipinos’ access to a diverse range of financial services beyond traditional banking. Digital banks and e-money platforms are positioned to further strengthen the Philippine banking infrastructure.

The result of this supply/demand imbalance is twofold: DRAM and NAND/SSD prices have risen sharply in recent months, and the availability of these components is limited, forcing device manufacturers to navigate a fluid situation.

Impact on global smartphone market

The global smartphone market, particularly Android manufacturers, is facing a threat in 2026. The industry’s decade-long trend of democratizing specs by bringing flagship features to affordable smartphones is reversing.

The cost structure of a smartphone is heavily dependent on the memory used. For a mid-range device, memory can represent 15-20% of the total bill of materials (BOM), while for a high-end flagship device, it is around 10-15%. As memory prices continue to surge, OEMs will likely have to raise prices significantly, cut specifications or both.

Manufacturers, whose business is mainly in the low end of the market, are likely to suffer significantly. The business models of vendors such as TCL, Transsion, Realme, Xiaomi, Lenovo, Oppo, Vivo, Honor or Huawei are based on thin margins. This increase in cost will hit their margins substantially, and they will have no other option but to pass the cost (or part) to end users.

Apple and Samsung face pressure but are structurally hedged. Their cash reserves and long-term supply agreements allow them to secure memory supply 12-24 months in advance. On the other hand, new flagship models in 2026 will likely have no RAM upgrades, sticking to 12GB for Pro models rather than increasing to 16GB. Current models won’t see same price erosion after introduction of the latest model.